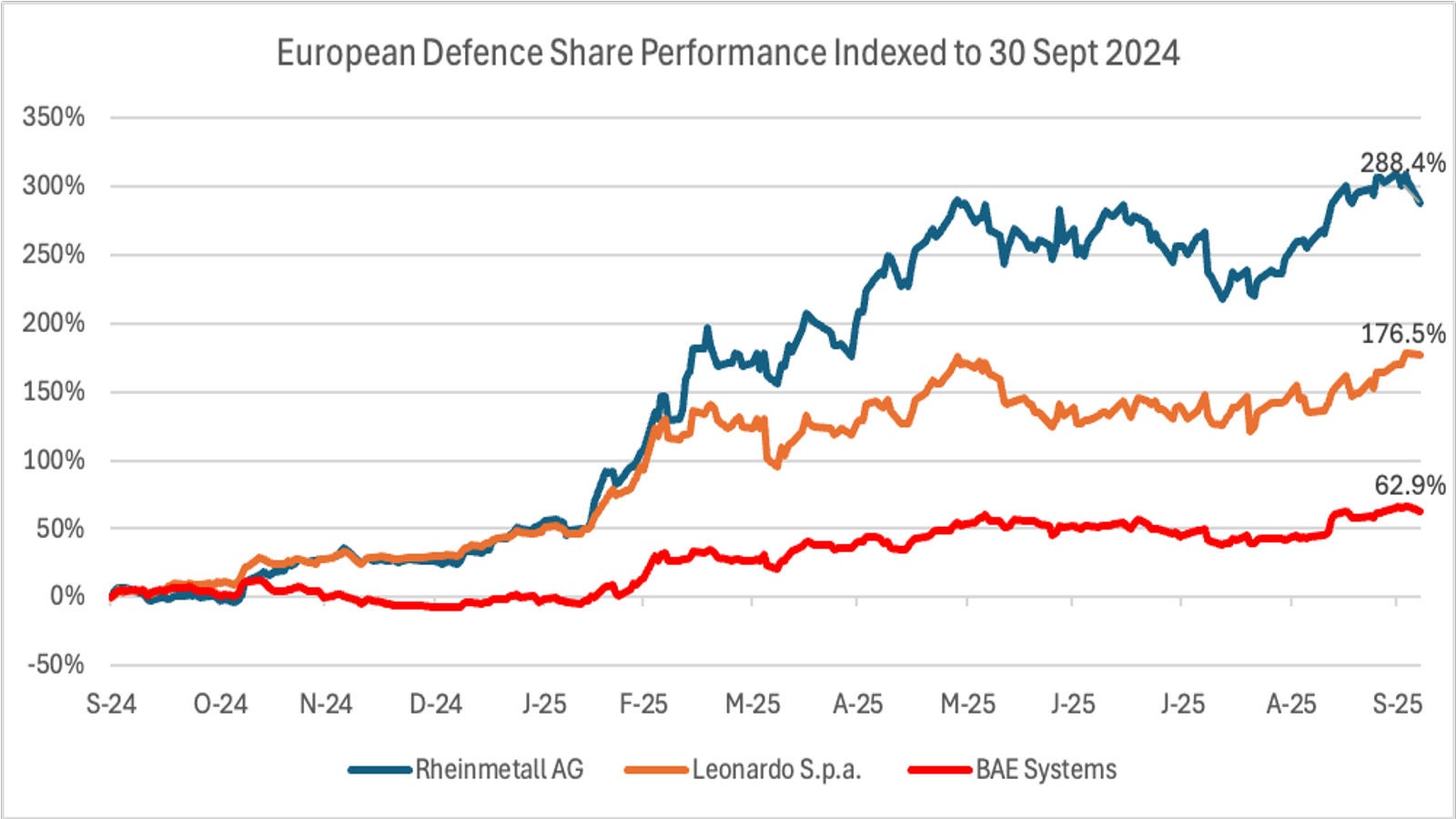

European defence stocks have soared this year, outperforming virtually every other sector. The space has garnered interest across the investment sphere from the rise of new defence ETFs and VC funds, to continued PE investment and oversubscribed credit issuances. Yet not without good reason, the three largest, pure-play defence primes in Europe have registered on average 127% returns YTD, extending on significant growth since 2022. In the case of Rheinmetall, this has translated into an extraordinary 21x return from 2022 to today, driven largely by Germany’s rapidly increasing defence spending and surging demand for ammunition.

Gains for European defence stocks from NATO pledge may face a reality check

Published: October 2025

Source: S&P Capital IQ (through 7 Oct 2025)

Following in-depth discussions with multiple industry experts, it’s clear that the defence industry is undergoing a paradigm shift that could change the economic and industrial make-up of Europe. Insights in this article are based primarily on information shared by Third Bridge experts:

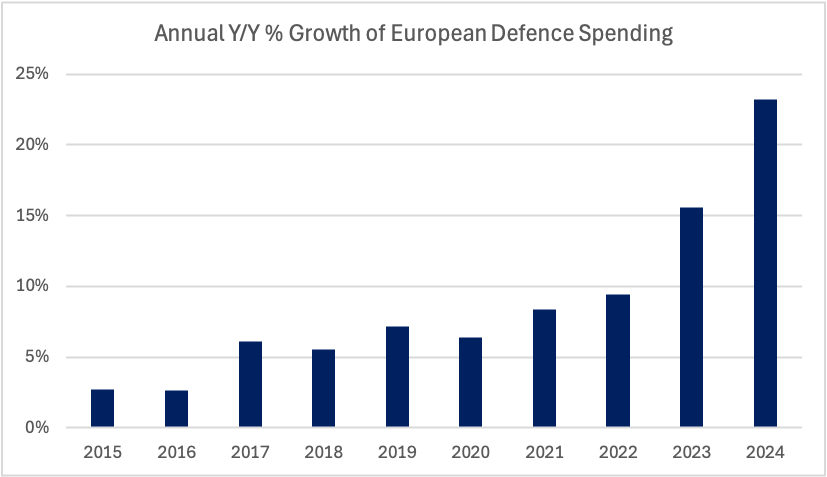

The Russia-Ukraine conflict has been a wake-up call for European Member States' defence spending. EU budgets rose from €333 billion in 2021 to €476 billion in 2024, and a further increase of at least €100 billion is projected by 2027. 1

US President Donald Trump called for fellow NATO member states to increase defence spending to 4% of GDP back in 20182, during which time the average NATO defence spending was 1.72% of GDP3 (excluding the US). His more recent and explicit demand for NATO members to spend 5% of their GDP on defence became widely reported, leading up to the June 2025 NATO Summit in The Hague. At this summit, NATO leaders formally agreed to a new commitment to invest 5% of GDP on core defence and security-related spending by 2035.

While NATO targets are not legally binding and act as guidance only, the European Commission's €800 billion ReArm plan and German Chancellor Merz’s signing of a law in April 2025 to loosen the so-called “debt brake” by exempting defence spending above 1%, from a constitutionally enshrined mechanism that limited government borrowing introduced in 2009 by Angela Merkel, are both indicators of real commitments to the target.

Europe has relied on the US for defence and security for decades, arguably since the signing of the Bretton Woods Agreement in 1944 – the post-WWII global monetary system designed to restore economic order underpinned by the nation’s military superiority, established largely through its nuclear show of power. Today, the US defence budget dwarfs its NATO peers at roughly 10x Germany, the second largest.3 This naturally means that there's a gap in what Europe can build, compounding the need for investment.

Capacity ramp-up limitations: A challenging reality

Despite a dramatic increase in defence spending commitments, Europe’s ability to rapidly scale up its defence production capacity faces significant and multi-faceted limitations. Third Bridge experts point to a history of low-growth, efficiency-focused operations that has left the continent with a depleted industrial base ill-equipped for a sudden surge in demand.

European defence has subsequently seen a record-level surge in order intake. Stock prices have rallied and high valuation multiples across the board now hinge on the successful deployment of large capital programs in an economy of often-depleted military assets and programs in Europe. These valuations ultimately rest on future cash flows, which in turn depends on Europe’s ability to deliver. The key question is whether it can deploy the CAPEX required to execute on their record order backlogs

Source: European Defence Agency

Ammunition production, for instance, is a critical bottleneck. Europe currently has five major nitrocellulose plants with a theoretical annual capacity of eight kilotons, but actual production is likely lower, despite the plants running at full utilization 24/7. Our experts highlight that scaling up is not as simple as building new factories. The process of restarting military production is a difficult task with new plants facing extensive legislative and regulatory hurdles, including environmental and safety issues. Obtaining licenses for a new site can take over a year alone. Moreover, a critical shortage of qualified, experienced technologists further constrains the ramp-up. Training new specialists takes years. While the EU and NATO have a target of reaching 20 kilotons by 2027, a more realistic timeframe is far later, and even that may not be sufficient to meet demand.

Similarly, in the land armaments sector, scaling up is capital-intensive. The lead time on the specialized machinery needed for expansion can be significant, sometimes taking 12 to 24 months to arrive, with additional time needed to integrate it into production. A major bottleneck in this sector is the testing and certification of ballistic steel, with limited approved suppliers and a certification process that can take over 18 months.

The disruption and impact of AI start-ups

The European defence landscape is being disrupted by the emergence of new AI start-ups. Traditional defence primes, historically focused on hardware manufacturing, are inherently challenged to excel in cutting-edge software development due to rigid pay structures and a lack of appealing work environments that would attract top tech talent. Their legacy systems, often built around a decades-long hardware cycle, are ill-suited for the rapid iteration and software-defined capabilities needed in modern warfare.

Third Bridge experts note that AI start-ups like Helsing and Anduril are capitalizing on this "tech gap”. They are venture capital-backed, which allows them to develop products and adapt their strategies much faster than traditional primes, who typically respond to customer demands and recover R&D costs through their existing customer base. These new entrants are not only developing software but increasingly creating vertically integrated products, such as drones, to overcome traditional procurement processes that are not set up to buy "off-the-shelf" capabilities. The Ukraine conflict has been a significant catalyst for this shift, as Western governments have been willing to quickly procure off-the-shelf equipment and rapidly iterate on what works in the field.

However, these start-ups also face challenges. The procurement process for defence is notoriously slow, with contracts taking years to finalize, which can be difficult for VC-backed companies seeking rapid returns. The ultimate success of these AI start-ups will depend heavily on the extent to which procurement reforms can truly change buying habits and procedures to a more multi-vendor approach.

Profitability driven by high demand, higher volumes, efficiency, and automation

The surge in demand for defence equipment is creating an environment ripe for increased profitability, according to Third Bridge experts, although the benefits may not be evenly distributed. For many primes and suppliers, the key to boosting margins lies in leveraging higher volumes and improving operational efficiency. For others it is in raising prices on the back of high demand and constrained supply, and favourable sole-source margin policy changes.

Defence contracts are often sole-source, which is the mechanism under which a defence department or ministry can award contracts without a competitive tender process. This can restrict the margin. However, with the current high demand, this situation is changing. Third Bridge experts see direct negotiation, as is common in sole-source scenarios, leading to a significant increase in margins along with a reassessment of the legislative frameworks themselves.

In the ammunition sector, for example, the price of artillery shells has tripled since the start of the Russia-Ukraine conflict for basic 155mm rounds where the shortage has been felt most strongly. Prices may not further increase, so the real profit driver is the increase in production volume. A factory with high fixed costs can achieve a bigger margin when it scales from producing 100,000 pieces to one million pieces with the same overhead. In some cases, profit margins on ammunition can be as high as 50% of turnover, with a capital expenditure payback period in months. This profitability, driven by increased supply shortfall, could be helping to offset rising raw material costs, such as nitrocellulose and steel.

Automation is seen as a way to enhance this efficiency, although its impact varies by sector. In ammunition production, automation is already widespread, with many factories being almost fully automated with robots. In the aerospace MRO sector, while maintenance remains largely a manual business, AI and digitalization are expected to improve processes like part recognition and in-service data analysis. However, in highly complex, low-volume sectors like tanks and artillery, automation is less of a differentiating factor. Instead, the ability to increase margins is more likely to come from direct negotiations and the urgency of a country’s needs, rather than economies of scale from automation.

The reliance of Europe on the US and the gap that must be filled

Europe's defence capabilities, particularly in sophisticated technology, have been heavily reliant on the US for decades. This dependence presents a significant challenge as the continent seeks to build its own sovereign defence capabilities.

A primary bottleneck in this area is the supply chain for microelectronics and high-speed processors. Most companies leading in this field, such as Nvidia, Xilinx, and Intel, are US-based. This reliance creates a vulnerability, as a withdrawal of US support or the imposition of tariffs could severely impact Europe's ability to develop and produce advanced systems. Third Bridge experts say the idea that US companies are inherently more sophisticated is not the whole truth. Rather, it is their historical consolidation of technologies over decades that has given them an edge. By consolidating its own isolated technologies and engaging in strategic mergers and acquisitions, Europe could become a formidable competitor.

The dependency extends beyond microchips to critical intelligence and communication systems, including satellites. While Europe has its own satellite capabilities through companies like Airbus and Thales, its network is not as extensive as the US's global infrastructure. Third Bridge experts say the political will to create a unified European defence strategy is a major hurdle. As different countries pursue their own projects a lack of "single European politics" leads to inefficiency making it difficult to achieve independence from the US. It will likely take several years to build the necessary infrastructure and even more time to develop the intelligence systems and political framework to share information effectively among European nations.

The drone revolution

The drone market, including unmanned aerial vehicles (UAVs) and unmanned combat aerial vehicles (UCAVs), is experiencing explosive growth, with a Third Bridge expert estimating a CAGR of 25-30% over the next 3-5 years. This growth is fueled by a significant capability gap in Europe, where most NATO countries have no dedicated attack drones, and a shift in military strategy highlighted by the conflict in Ukraine. The conflict demonstrated the mass adoption of low-cost drones for surveillance and strike missions, and the high effectiveness of loitering munitions against armored vehicles.

According to Third Bridge experts, a significant area of development is "manned-unmanned teaming”, where a single fighter jet can be accompanied by a fleet of "loyal wingman" drones, dramatically increasing combat mass and capability at a lower cost. The counter-drone market is also booming as a direct response to this threat, with new technologies like microwave weapons and laser systems being developed to neutralize mass drone swarms. While Europe is currently considered "bare naked" in terms of drone fleets, the industrial capacity for smaller drones is not a major challenge, as airframes are relatively simple to build. The main hurdles are securing the supply chain for key components and the need for a political environment that encourages long-term investment.